Choosing an Amex Card

As Kyle wrote last week, we are losing most of the benefits of our current primary rewards card. We will still have our Chase Freedom card, which gives 1% on most everything and periodically 5% in certain categories. When those 5% categories coincide with our purchases we will use that card, but the rest of the time we’ll likely use whatever our new primary card is, especially if our rewards are above 1%. It would be nice if we could replicate some of the rewards categories we are losing (gas, travel) but we would certainly be open to different rewards.

Simultaneously, we have realized that we have been spending quite a lot of money at Costco – it was actually the third largest single merchant recipient of our money last year after our apartment complex and Delta! So we thought it might be nice to get a little bit of rewards out of all that spending by getting an American Express card, the only credit card brand accepted by Costco.

The three main Amex cashback cards that we are considering are the Costco card, Blue Cash, and Blue Cash Preferred. The last has an annual fee of $75.

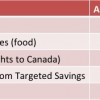

Here are the rewards percentage breakdowns:

To assess which card would maximize our rewards, we assume that the future looks like the past. We also assume that this card would function as our primary card, with the Chase Freedom card only taking away rewards during certain periods and not asymmetrically affecting the rewards generated by these cards.

Using Mint, I found our spending levels in the last year in all the relevant categories. Then I multiplied by the various reward percentages to see how much each category of spending would contribute to the rewards for each card. Here are the results:

Note 1: Macy’s (affiliate link – thanks for using!) is the stand-in for “department stores.” I don’t think we’ve used any other department stores. Note 2: The spending labeled “grocery stores” does not include groceries from Costco or Target (which apparently doesn’t count as a grocery store). Note 3: The total rewards for the Blue Cash Preferred card has the $75 annual fee subtracted.

The conclusion here is that the Costco card would generate the most rewards for us, so if we are going to apply for only one new card that should be it. $150 in a year doesn’t seem like much, but hey, it’s free money without changing our habits at all.

P.S. Mint is awesome for making looking up these numbers so easy!

Do you have any of the cards I analyzed and how do you like them? Do you prefer cashback rewards cards or other types? Do you use your past spending records to predict the future?

Filed under: credit cards · Tags: American Express, Blue Cash, Blue Cash Preferred, Costco TrueEarnings

Why We’re Not Getting the Chase Sapphire Preferred Card Even Though It’s a Great Deal

Why We’re Not Getting the Chase Sapphire Preferred Card Even Though It’s a Great Deal “I Want a Credit Card, But I’m Scared”

“I Want a Credit Card, But I’m Scared” Putting Rent on a Credit Card: An Opportunity to Churn

Putting Rent on a Credit Card: An Opportunity to Churn Don’t Buy into the Pro- or Anti-Credit Card Hype

Don’t Buy into the Pro- or Anti-Credit Card Hype20 Responses to "Choosing an Amex Card"

Leave a Reply

Recent Comments

- Adam on Home Equity Is Funny Money

"Hi Emily - I just stumbled upon your blog. Great post! Up in Canada this is a…" - Emily on Home Equity Is Funny Money

"I agree that an appraisal is the best number to work with. I can't think of why …" - JL on Home Equity Is Funny Money

"I only note it as round numbers, in $50k or $100k estimates. I also usually upda…" - We Maxed Out All Our Retirement Accounts for the First Time! - Evolving Personal Finance | Evolving Personal Finance on Avoiding an Expensive 401(k) Plan through Self-Employment

"[…] was the first year that we contributed to Kyle’s expensive 401(k…" - Business Goal Tracking for Week 8 of 2022 - Evolving Personal Finance | Evolving Personal Finance on Business Goal Tracking for Week 6 of 2022

"[…] Done as of two weeks ago! […]…"

Very well done! You’re so analytical and I love it! Numbers don’t lie and this pretty much shows you your answer.

It also shows the Blue Card is not a good deal and especially not worth the $75 annual fee.

sorry to be lame but I don’t have any reward cards. We don’t spend any money…lol

If we spent a bit more it might tip in favor of the fee card, but then I’d have to take into account the quarters where we’d be using our Chase Freedom card, which would limit rewards generated with the Amex… I’m glad the initial numbers didn’t point that way.

I feel like we don’t spend any money but we put everything possible on credit cards so it adds up a little.

I don’t use Amex because I’m Canadian but I definitely prefer cash back rewards. I usually go online and total up how much I’ve spent to see how much I’ll get back after the year is over.

I like Amex SPG and Amex Hilton Honors if you stay in those hotels. Wait for a big sign-on bonus (25,000 SPG points or above) if you are applying for hte SPG one. It’s $65 annual fee but the first year is waived.

Sounds like a good deal but we only stay in hotels 1-2 times per year, which is part of why we prefer cashback cards. When we travel we are almost always able to stay with family or friends.

I like the way you have put forward your analysis.

Sounds great! Mint seems like a great system…still haven’t used it yet, tho. I always throw away offers for cards with annual fees, but I guess I should do something like this first to see if it’s worth it.

We didn’t get an offer but rather are searching for another card and decided to consider the preferred card as well, although it would take a lot to convince me to pay an annual fee!

We love Mint but it’s not perfect. For this kind of analysis I think it’s very powerful.

Great way to shortlist a card. Nice example, going in to my round up tomorrow

Thanks SB!

[…] Which Amex card is best? Emily of Evolving Personal Finance tells you hers. […]

[…] PF has an comprehensive post about choosing the right kind of credit card according to your shopping habit. I have been tell people to do exact same thing on my other blog […]

I love this little break down! I generated something similar and it’s a great way to see which card (or combination of cards) work for your already-established spending choices.

But now I’m curious…do Costco purchases not count as “groceries” under the Amex Blue Cash cards? Seems like they should, which would allow you to save either 3 or 6% (depending on if you go with the standard or preferred card) rather than just 1% for that card’s breakdown.

I guess you’d have to see how much you’re saving by going to Costco over regular grocery stores, but seems like you could get 6% x (2605+1012 = 3617) – 75 = 142.02 back (from the groceries alone)using the Blue Cash Preferred, and then with the other categories save over $200 each year–a better deal than the Costco TrueEarnings card. Am I doing the math right? If so, we might look into the Blue Cash Preferred card…

Correct, Costco and other warehouse-type stores do not count as grocery stores.

I’m in the midst of a detailed grocery prices analysis involving our local grocery stores, Costco, ALDI, and our CSA now that it has started. I’m willing to bet that the rewards could not overcome the price differences between Costco/ALDI and the grocery stores, but I don’t yet have data to support that. I may conclude that we need to switch to ALDI as our primary store, which would eliminate all rewards but probably save us a lot of money. I sort of wish we hadn’t just renewed our Costco membership.

I see–that makes sense they’d want to incentivize other savings cards specific to those stores.

The grocery analysis will certainly be interesting to read about. I look forward to that!

[…] few months Kyle and I consider adding a credit card to our collection to further optimize our rewards. Most of the time we […]

[…] use rewards credit cards whenever possible – we largely go for cards that will give us long-term rewards but occasionally will churn a card with a great sign-up bonus and a minimum spend requirement we […]

You’re missing an Amex that would actually be more worth it than the three you listed: the Fidelity Investment Rewards Amex. It gives you 2% cashback on every purchase and if you open a Fidelity account, you can cash out after $50 in cashback. Based on your spending listed, it would have earned you $180.60 in cashback last year. That’s not a bad card to use as your only one then!

Leigh recently posted..Association between your job and paying the bills

Hey, thanks for the tip! I didn’t look at all the available Amex cards.

[…] choice of card, like gas. I definitely wouldn’t be opposed to adding another card or two – an Amex one to use at Costco or one that offers a sweet signup […]