How to Make an Irregular Income as Regular as Possible

One of the clients I coached recently wanted to talk over how to handle his irregular income. He was having trouble sticking to his budget because he ran his own business and his income fluctuated month-to-month. I read a bunch of blog posts on the subject and my client found the strategies I suggested helpful, so I thought I would put all of it together in a blog post – with whiteboard drawings!

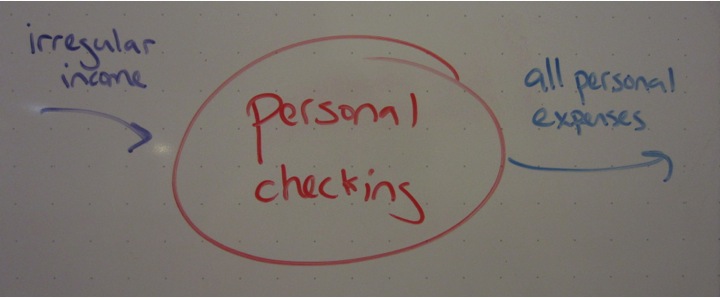

Here’s what it boils down to: Use separate checking accounts to smooth out your income. Gather all of your irregular income into one account and then pay yourself (i.e. to your personal account) a regular salary. The more your income fluctuates, the more this strategy will help you facilitate a regular budget out of your personal checking account.

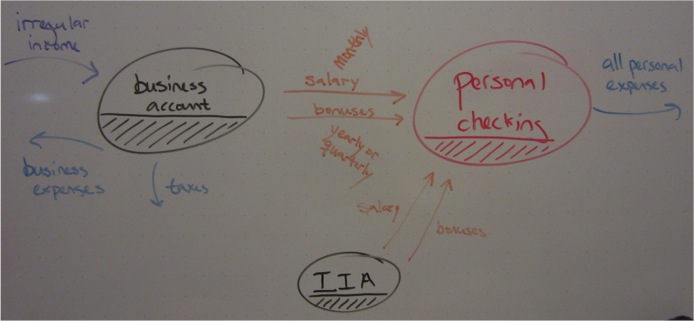

1) Open at least one additional checking account into which you deposit your irregular income (IIA). If you run your own business, you must have a business account that is separate from your personal checking. This will make keeping track of your business income and expenses much easier and your accountant will thank you come tax time.

2) Pay yourself a salary from your IIA that is somewhere between your minimum and average monthly income (after taxes and expenses). Build your basic monthly budget off this salary.

3) Build up enough buffer in your IIA so that you can sustain the salary you chose even if you have several consecutive lean months – for instance, six months to one year of the difference between your salary and the minimum you make in a month. If this is for your own business, there should also be enough buffer to account for the temporary expenses you may incur and for taxes.

4) Pay yourself bonuses between once per year and quarterly. Since you don’t need these bonuses for your regular budget, you can use them as extra short-term or long-term savings or to make large purchases/splurge. If your income falls below your projections, you can forgo these bonuses. The balance between the size of your salary and your bonuses is something that you can play around with, but be conservative with your bonuses when your buffer is lower and you have more uncertainty about your income.

5) (Optional) You can use this strategy for each independent income stream you have, if you like (and certainly for every business you run). If one of your sources of income dwarfs the others this may not feel necessary, but it just depends on how regular you want your income to your personal account to be.

Like many other topics in personal finance, there are simple and elegant solutions to problems – the difficulty is in implementation! I imagine it’s very hard to project one’s income, especially if your income is dependent on commissions (or other people’s decisions generally) and there’s not much you can do to make up for a shortfall in a given month. On top of that, deciding how much salary to take, especially at the same time that you may be launching a business, must be very difficult. But even if you can’t work this system perfectly from the beginning, any shift away from putting all your irregular income into your personal checking account and into an IIA will be helpful in keeping a more regular budget.

Blog posts I found helpful: 99u, Simple Mom

What’s your strategy for irregular income? (We don’t actually have any so please critique the strategy I outlined!)

Filed under: income · Tags: budgeting, irregular income, self-employment

Irregular Income: Gravy Edition

Irregular Income: Gravy Edition Irregular Expenses Are Still Kicking Our Butts!

Irregular Expenses Are Still Kicking Our Butts! Living on One Income: What to Do with the Other?

Living on One Income: What to Do with the Other? How to Budget from a Lump Sum of Income

How to Budget from a Lump Sum of Income30 Responses to "How to Make an Irregular Income as Regular as Possible"

Leave a Reply

Recent Comments

- Adam on Home Equity Is Funny Money

"Hi Emily - I just stumbled upon your blog. Great post! Up in Canada this is a…" - Emily on Home Equity Is Funny Money

"I agree that an appraisal is the best number to work with. I can't think of why …" - JL on Home Equity Is Funny Money

"I only note it as round numbers, in $50k or $100k estimates. I also usually upda…" - We Maxed Out All Our Retirement Accounts for the First Time! - Evolving Personal Finance | Evolving Personal Finance on Avoiding an Expensive 401(k) Plan through Self-Employment

"[…] was the first year that we contributed to Kyle’s expensive 401(k…" - Business Goal Tracking for Week 8 of 2022 - Evolving Personal Finance | Evolving Personal Finance on Business Goal Tracking for Week 6 of 2022

"[…] Done as of two weeks ago! […]…"

This is actually a good idea. My boyfriend is self employed and so he has somewhat of an irregular income but we make enough to handle all of our bills and save some too, so it’s not that big of a deal. He just puts excess into savings.

But I can see how that must be very stressful for those who have very little income one month and way more the next.

Daisy recently posted..The Life Insurance Movement: I’m Indifferent

It’s great that you have the self-control not to inflate your lifestyle to meet his irregular income, even on the lower side. I think the system I outlined would help people who are more willing to spend everything that ends up in their checking accounts.

I really like this idea! My income isn’t as irregular as some, but I get “supplemental comp” from my superiors in one paycheck per month, as well as other random incentive-based bonuses. This has taken me a while to get used to, and I have been advised to *never* count on the extra stuff and base my budget around my base salary. As the years go on this has become impossible since my “supplemental comp” is now 1/3 of what I make, so I have to factor it in when it comes to figuring out, say, how much house we can afford.

This strategy of yours seems very smart. What I might try is having my paycheck deposited directly into my savings account, and then paying myself from savings to checking a consistent amount. Thank you for getting me thinking!

That sounds like a great idea! You really don’t need the second account to be checking unless you’re running a business and you have to spend money out of it. Now that your extra income is such a large fraction of your total income it does make sense to factor it into your planning even though it’s uncomfortable. If you have a big buffer, though, you can pay yourself money that came in months ago so you have room for adjustment if the future extra income doesn’t come in.

Great article! The way you lay it out makes the process seem like a no-brainer, but I know it’s a challenge that a TON of people face!

femmefrugality recently posted..How to Pick a Major Without Wasting Money

It’s difficult to say much more about this until you get into the nitty gritty of someone’s situation! The big picture is easy but deciding on the salary would be nerve-wracking.

Whew…I can see how this can be complicated for people! I’m really glad I know how to budget and learned fairly quickly how to handle my irregular income. Great tips though Emily! I love the idea of the annual or quarterly bonus. Hopefully I can earn enough to justify that. 🙂

WorkSaveLive recently posted..Recipe: Vegetarian Bolognese

This is pretty close to what you described in your irregular income post last week, right? Except that you start with the buffer and work back to the salary/bonuses?

As a server and a freelancer, all of my income is variable, which is quite annoying ! Thanks for the info.

Drop that Debt recently posted..Free Activities

Do you think you’ll implement this strategy? If you realize you have a lower-income month, are you able to work more to make up for it?

Hmmm I might have to try this. I have been hesitant to get into budgeting mostly because of my fluctuating salary. I could see this really helping prevent lifestyle inflation during times when you suddenly have extra in your bank account.

Modest Money recently posted..5 Places You’re Not Looking for Content Ideas

I agree. It still leaves the motivation to work hard because of the bonuses, but it’s something that you can plan ahead for to prevent lifestyle inflation, like you said.

That’s a really good strategy – I like the option of paying out bonuses every so often. I think this is what I would like to do as we grow our irregular income streams, it’s jsut like being employed at a second job!

Brian recently posted..Seeing Washington, DC – Free!

I would employ this strategy if we had any irregular income. 🙂 If we ever monetize this blog we’ll definitely have all that income go into another account until we decide how to pay ourselves from it.

I love this — my “irregular” income is not very much, so that almost always just gets added to the “debt du jour” payment that month. Next, it’ll go toward savings, but it’s never money I’m counting on.

Kathleen @ Frugal Portland recently posted..Santa came early!

If you don’t depend on your irregular income source, this strategy is probably overkill. Having a goal for all of the irregular income is a great strategy until it becomes a significant fraction of your overall income.

This is along the lines of what I’ve been doing for the tiny amount of online income I make. It all goes into a savings account and then once per month I move the money I need out of the savings into my checking.

My day job is pretty irrgular, as well. In that case, similar to what you said, a certain portion of each pay check goes into my checking account. That more or less covers all of my personal expenses. The rest goes into the joint savings account.

Sounds like you came to the same solution without necessarily planning on it, which I think means it’s a robust system.

Flow charts and white boards – this is my kind of post! That’s actually pretty good advice. I don’t have irregular income, but if I did I would use a strategy like this to keep my sanity.

My Money Design recently posted..Asset Allocation Models from Author Daniel Solin

Thanks! I LOVE my whiteboard.

This is a good strategy, and is what I would do if I had enough regular side income to make a difference. The key here would be the setup – you can do basically everything automatically after that, but the set up would need to be spot on.

Jeff @ Sustainable Life Blog recently posted..Honeymoon: Japan

I agree. It might take a bit of tweaking at the beginning – salary/bonuses – but the more stability you let it give you the better!

This is a little dissimilar, but close to what I do. Basically I get all of my income direct deposited to my personal checking account, whether regular paychecks, side income, or grant money (we’re talking small time help with travel here, not $5 million NSF grants!), and then move what we *don’t* need for basic expenses or regular savings goals to a savings account just for summer living and research expenses. This works because my income is regular 75% of the time – I think your system would work better for someone self employed with constantly irregular income, or for someone who just didn’t want to figure out how much went into which “buckets” every time. During the summer or during research travel I just transfer what I need into checking on a monthly basis, but this summer so far we haven’t needed to take as much out as I expected, so that is neat.

What is the purpose of “bonuses”? Not everyone on a salary has bonuses, why is that something a self employed person would wat to work in?

I think the system is also helpful if you don’t want to will yourself to transfer money out to savings once it’s already appeared in your personal checking!

The bonus aspect is just to account for the irregularity, really. Once you have enough buffer and you’ve established a sustainable salary level that is below your average, you’re still going to have money accumulating in your IIA, just at different rates throughout the year. So if you have a really good year or quarter or whatever you can reward yourself afterward with a bonus (or give yourself a raise if you think the increase is sustainable).

[…] How to Make an Irregular Income as Regular as Possible at Evolving PF […]

[…] from The Family Finances listed How to Make an Irregular Income as Regular as Possible in his friends of the […]

[…] 1) How to Make an Irregular Income as Regular as Possible […]

[…] How to Make an Irregular Income as Regular as Possible by Evolving PF. […]

[…] (that we later found out was paid) so that he could learn a new skill. While I still stand by the method of handling irregular income I outlined earlier, that strategy is for people who depend on their irregular income for their normal living expenses […]

[…] size. For instance, self-employed individuals may want to keep more savings on hand to practice income smoothing. Certainly anyone who can anticipate the likelihood of an emergency, like a job loss or a baby on […]