Diverted from the Slope

I swear, I wasn’t trying to test my husband. I honestly was reconsidering our TOTALLY JOINT MONEY arrangement for Kyle’s sake. My personality as drifted further toward “saver” since I became financially independent from my parents and I’ve imposed those tendencies on Kyle to a great extent since we got married. Kyle is a saver as well but he enjoyed buying electronics and making some small impulse purchases before we were married and those purchases have slowed considerably.

In the last few months I’ve wondered if I’ve kept too tight a rein on our budget. We still have a monthly autowithdrawal into our Electronics savings account but it’s fairly minor and we’ve all but eliminated fast food and last-minute-dining from our life. I’ve worried that Kyle is lying dormant now, under pressure, but will soon erupt in a frustrated spending spree.

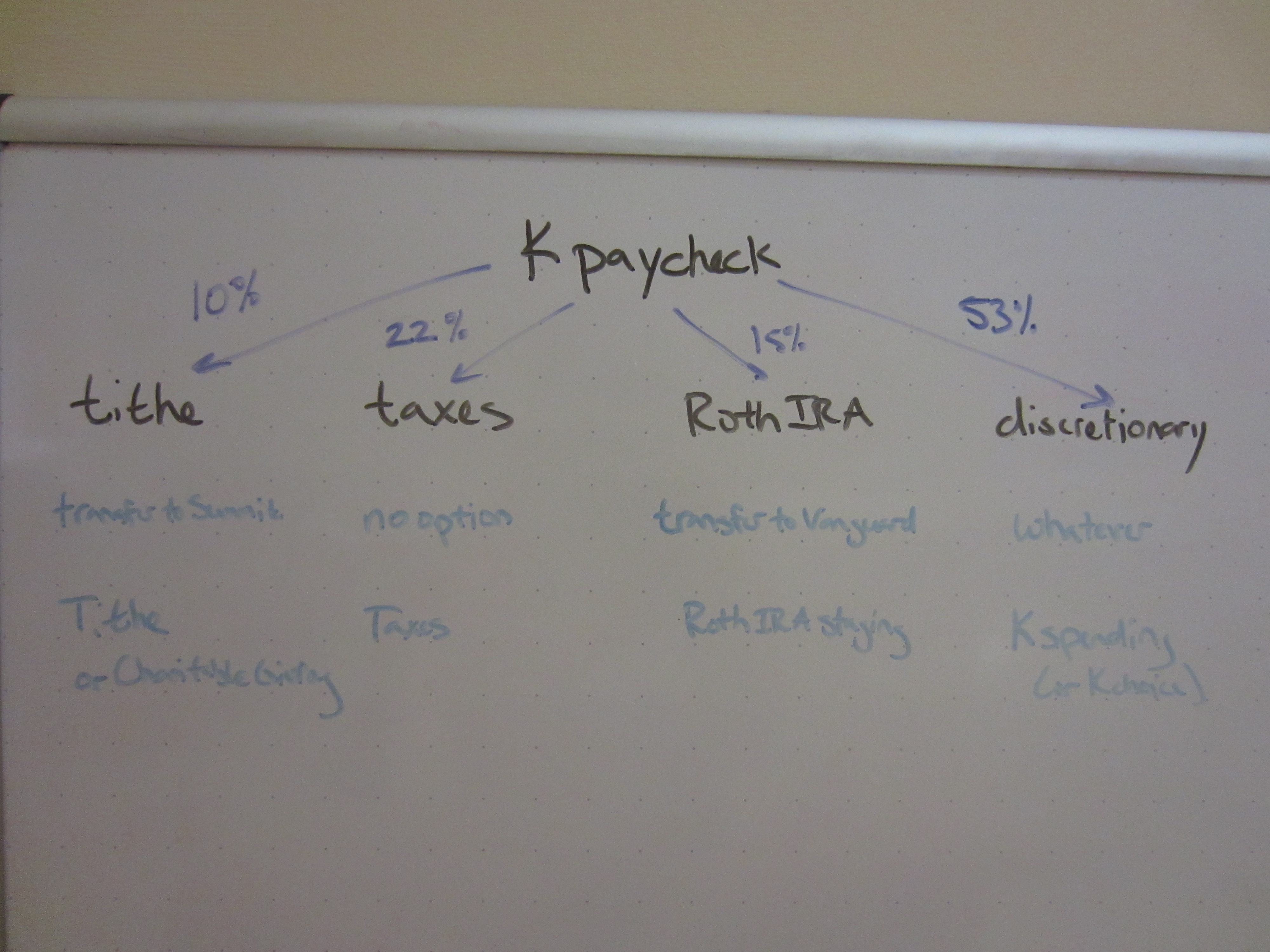

Kyle trained all summer for a part-time position at our church, and this month he finally got his first paycheck. This past weekend I put together a proposal for what I would like to do with the money: after meeting all of our percentage obligations, we can open up a new savings account just for Kyle and put the remainder of the money there so that he can spend whatever accumulates there however he wants..

Up until now it has been easy to have totally joint money (all joint accounts, no separate allowances even) as our stipends are nearly identical and we have very similar money personalities. Cash birthday presents have presented us with challenges to our joint money mindset but nothing like this additional straight-up-time-for-money paycheck. Kyle has worked really hard to qualify for this job and has to get up super early on the weekends to perform it – shouldn’t he get to spend the non-obligated money however he wants? I don’t feel the need to have my own individual money but perhaps Kyle does.

Thankfully, Kyle pulled me back from the brink of the slippery slope of separate money. An individual savings account for him would have led to his and hers clothing and toys and food separate money and who knows how to stop that train. Kyle told me “No separate money! Let’s just put it in Electronics.”

A man after my own heart. 🙂

Have you ever been tempted to separate part of your money from your spouse? Does a salary feel different from sidle hustle money? If you have any separate money, how do you decide what is joint and what is separate? Has your spouse saved you from making any terrible decisions recently?

Filed under: marriage, side income · Tags: joint money, separate money, side hustle

The Slippery Slope of Separate Money

The Slippery Slope of Separate Money Realities of Account Ownership

Realities of Account Ownership Found Money Creates Wants

Found Money Creates Wants Money Management Systems Visualized

Money Management Systems Visualized32 Responses to "Diverted from the Slope"

Leave a Reply

Recent Comments

- Adam on Home Equity Is Funny Money

"Hi Emily - I just stumbled upon your blog. Great post! Up in Canada this is a…" - Emily on Home Equity Is Funny Money

"I agree that an appraisal is the best number to work with. I can't think of why …" - JL on Home Equity Is Funny Money

"I only note it as round numbers, in $50k or $100k estimates. I also usually upda…" - We Maxed Out All Our Retirement Accounts for the First Time! - Evolving Personal Finance | Evolving Personal Finance on Avoiding an Expensive 401(k) Plan through Self-Employment

"[…] was the first year that we contributed to Kyle’s expensive 401(k…" - Business Goal Tracking for Week 8 of 2022 - Evolving Personal Finance | Evolving Personal Finance on Business Goal Tracking for Week 6 of 2022

"[…] Done as of two weeks ago! […]…"

I do have a sepearte checking account. It’s primarily for my debt payments as their variable due dates always frustrated her. $100 from my paychecks, plus all of my other income streams ($200-300/month) go in there. Mostly I’m letting the extra pile up for a baloon payment at the end of the year. The original plan was to pay off my last credit card with that payment, but I didn’t make anywhere near as much this year as I had planned. But the understanding is that if I want to spend more than my budget for “me” money, I have to do it out of my own pocket.

Incidently, the rest of my paycheck goes into a joint savings account that is used for short/medium-term savings goals, such as our down payment or a new tv. My wife’s paychecks go into our checking account and cover all of our regular expenses, plus a little extra.

Edward Antrobus recently posted..Saving Money With Two For One Deals

Variable due dates would frustrate me, too! Once you have your debt paid off what’s the joint/separate plan?

To be honest, I haven’t thought that far ahead. Unless I get a lot better at bringing in side-income, that’s about 7 years away yet. At that point, I’ll probably close my checking account and let the money pile up in our joint savings while we try to figure out how to spend all that money.

Edward Antrobus recently posted..Places I’ve Been: Week Ending Oct 13

Money is complicated! We moved to joint + allowances to make things easier so we wouldn’t always be asking “is this purchase joint or individual,” but it still happens sometimes.

For instance, it turns out I’m a bigger spender than my husband, in that my allowance isn’t enough to pay for my once or twice yearly haircuts, or a new pair of shoes, without saving up and skipping out on happy hours and entertainment for a long time (which is the purpose of the allowance for both of us). But those have been part of “personal spending” in part because they do cost me more – husband buzz-cuts his own hair over the bathroom sink for free, and can get away with wearing sneakers to work daily, which doesn’t seem appropriate in my field. Also, since women have to meet different expectations of appearance than men, it’s hard to draw the line between “wants” and “needs” sometimes. I am pretty sure that if I were to say “hey, can I spend joint money on a haircut” the answer would be “yeah, no problem,” but I haven’t yet.

I’m not sure this is something that totally joint money would fix, though – it would just turn into guilt over spending “our” money frivolously for “my” purposes, whereas at least allowances release us from worrying about if a purchase is useful to the other person! Sounds like ugly feelings but they come out of a place of wanting to protect the other person’s interests and not take advantage of them. How do you and Kyle avoid this problem if, say, he DOES want to buy some electronics that you wouldn’t use?

My working out of state, and keeping separate grant and side hustle money to pick up a lot of those costs, has been another headache, but a necessary one. We’re hoping we can get a subletter for the spring to help with that, although our apartment isn’t really a 2-bedroom so we couldn’t ask market price.

Whew! Long comment. I guess the gist of it is…how do you manage complex and asymmetrical needs, with OR without totally joint money?

I have had all the same thoughts as you over this issue at least for our joint money, and considering what we would do differently if we had separate money (answer: too much).

We haven’t said this explicitly to each other in the context of joint money, but here are three principles we use:

1) Our marriage comes before our individual preferences.

2) Fair does not necessarily mean equal.

3) Give grace if you want to receive grace (i.e. the golden rule).

Basically, we trust each other to delineate between our own wants and needs (and needs-that-we-want-to-upgrade). If one of us needs something – yes, haircuts, clothes, electronics – we buy it. Our joint budget provides room for all needs and upgraded needs. As for wants, we talk it over and look at our account balances and often the person bringing the want to the table will withdraw it if there are higher priorities. Kyle isn’t really qualified to judge what clothes I need and how much I need to spend, for instance, because of the differences between expectations of men and women like you mentioned. He trusts me to self-regulate. Likewise, Kyle just likes fancy gadgets a lot more than I do and I don’t want to make him live in agony or whatever because he doesn’t have something that in his world is pretty much a need. He also self-regulates very well – he has been without a smartphone for almost two months now and is still researching his options! He knows where the money will come from and so can judge if what he wants is the best use given our whole financial picture. He wouldn’t force me into a big purchase if I wasn’t comfortable with, but we’re both working off the same information, you know?

I definitely understand there might be some tension over things that are the exclusive use of one person or the other, but I wouldn’t feel guilty over using our money for something just for me. My well-being contributes to our marital well-being, after all.

I think this approach is easy for us because we have such similar money personalities (though different preferred spending areas), we have big joint priorities (travel), and we keep a tight budget to begin with.

Yeah, that all makes sense. This is way more an issue of my not trusting myself to tell “wants” apart from “needs” than him not trusting me, because we both definitely presume each other’s good faith. I suspect some things simply get easier with cash flow as well, no matter your money management system; when your budget is a bit less tight, getting a haircut does not feel like it “costs” so much in tradeoffs.

I imagine having more cash flow will make these discussions more difficult, actually… I don’t feel guilty about spending what I need to but we might have more yours-vs.-mine tension when we are able to meet more wants.

We have a joint budget/spending plan and joint goals for our money, but all of our accounts are still individual. I think we’ll keep it this way forever- but maybe we’ll combine if/when we have kids or one of us becomes a stay-at-home parent.

Eventually when we’re both working we’ll establish a joint account for our joint payments- housing, auto, insurance, etc., and then contribute relative to our individual incomes (so, if I’m making 75% of our total, I’ll put in 75% of the contribution to the account).

There are no secrets-we do our banking side-by-side, so I really don’t see the difficulty with keeping it separate.

SWR recently posted..Our holiday travel plans

I don’t think keeping separate finances is technically difficult either (or requires any more or less trust than joint).

Everything of ours is joint. It works for us because I can help keep him in check even though he is a CRAZY spendy spender.

Michelle recently posted..Glad I’m Done With School

How do you keep him in check? Is it enough to notice his spending?

We have finance “meetings” and talk about our money a decent amount. He knows that he needs it because he isn’t good with money.

Michelle recently posted..Why Does It Always Rain When I Travel?

That’s pretty much how we work it too Michelle!

eemusings recently posted..Link love (Powered by tiramisu and the Muppets)

Wow! You almost went over the cliff! I liked your story. It shows why you’re such a great couple 😉

AverageJoe recently posted..How I Saved 35% on My Walt Disney World Vacation

Aw, thanks Joe.

My bf and I cohabitate, so we aren’t married, but I have a hard time imagining myself sharing ALL of the money once we are married. It might just be our personalities, but we never fight about money. We split our fixed expenses and then have separate accounts for our flex spending. When we go on vacation he puts it on his credit card and I just pay him for half of it. It’s not the best or most involved method, but it works for us 🙂

L Bee and the Money Tree recently posted..Top 10 Money Saving Tips I Learned from my Grumpy Father-in-Law

Sounds like pretty standard partial pooling.

We don’t have any seperate accounts and it works well for us. The only exception is that if one of us gets money or a gift card for birthdays/Christmas then we spend it how we want. Other than that, we make all financial decisions together. It works well!

Holly@ClubThrifty recently posted..How to Be More Credit Savvy

Usually how I want to “spend” cash gifts is to just put it into short-term savings (whatever needs the most help at the moment) but Kyle spends it on himself… so there was a bit of tension last time it came up. I’m being a bit unrealistic, though!

We have our own separate fun accounts (aka allowance, blow money, etc) and then what we call our “mutual fun” account. The individual accounts take care of things like going out for lunch at work, buying tools and electronics (me), expensive haircuts (her), or anything else that we want to spend on ourselves. The mutual fun account is for vacations, eating out together, date nights, etc.

So far it has worked out well for us. We may decide to increase or decrease specific accounts based on how they’re working over the long run, but for now it seems to be working well.

I like your point that fair doesn’t always mean equal, for example my wife has to fulfill a certain numbers of continuing education credits (she’s in the medical field) that aren’t covered by her job (basically a forced pay cut) so rather than arguing about it each time it comes up we created another account for continuing ed. It’s certainly not equal, but it wouldn’t be fair to her to ask her to pay for it.

Aside from the individual fun accounts, we agree that anything else should be together. Haircuts may eventually fall under the together category, although I’m like “Emily too”s husband, I cut my hair with a clipper in the bathroom.

Great post.

David@SkepticFinance recently posted..Are Prepaid Phones Worth It? (Part 1 of 3)

I like the specificity of your system. I just think if we tried to separate anything we wouldn’t know where to stop… And I don’t mind checking in with Kyle when I need to spend some money. We share a car anyway so it would be pretty difficult for one of us to make a purchase without the other knowing!

Hair is one expense that I can see going to either gender for typical greater spending – I get really cheap haircuts so if they’re infrequent enough Kyle would outspend me in that area. Except now I cut his hair, which is a fund bonding experience (except when I screw up!).

I’m not sure you were in any danger of sliding down a slope into splitting a plate of french fries based on who ate more! But I like his response — electronics are his thing, anyway, right?

Kathleen @ Frugal Portland recently posted..Overheard at the Office

Well, our next two purchases from that account are going to be a smartphone for each of us, so… not exclusively. 🙂 And any other device he might buy I would use at least part of the time.

Oh and believe me, Kyle eats ALL the French fries!

We deal with these issues by DH having an allowance.

Nicoleandmaggie recently posted..When I am an old tenured woman

I guess the conclusion was that I was creating an issue out of nothing since Kyle is much more able to handle the tight budget than I gave him credit for.

How did you decide to do a unilateral allowance? We’ve talked a lot about “fairness” in this post so how do you think that relates to the allowance?

http://nicoleandmaggie.wordpress.com/2011/01/17/in-praise-of-dhs-adult-allowance/

nicoleandmaggie recently posted..What the allowance does

He wants to keep it all together! And actually we recently came up with another idea for his side hustle money that both of us will use.

[…] INCOME: Same as last month from grad school, plus Kyle got a small paycheck for his side hustle. […]

[…] 5) Diverted from the Slope […]

[…] we agreed he should be the one to decide how to use this portion of the income (of course toward shared spending). He chose for the gravy gravy to go into our Travel account at the present. I think this is a […]

One day my BF and I will share this stuff, but at the moment, we just pay in turns for meals out etc. Interestingly, we talk about other people’s money and spending habits a bit – cause ours are so similar. We both feel annoyed if we spend a lot, and devalue some items over others (and then spend money where others wouldn’t ‘waste’ it – like coffees!) I can’t wait til we get to the point where we share savings goals – but how is a big hurdle to get over first, so everyone comments are really interesting

SarahN recently posted..Ways I ‘spend’ money

No reason to rush sharing finances! It’s a super-important decision and step. Kyle and I were transparent in our finances before we got married and joined them, but it took several years to get to that point.